If you’ve had to buy anything lately, you’ve probably noticed that just about everything is more expensive now than it was this time last year. It’s not just you — inflation has caused prices to rise across the board. But it’s about more than the costs of goods and services.

Inflation has a way of extending beyond the price tag, including impacting the overall health of the system and the individuals who receive benefits.

You’ve probably heard that Social Security is going broke. Given that, it’s logical to ask, “Why can’t the government just print more money to fix this problem?”

That might sound like the simple and obvious solution. But there are good reasons why printing money to fix this problem isn’t the outcome that any of us want. Doing so could lead to some serious unintended consequences.

The Social Security cost of living adjustment is seemingly straightforward. But, like most provisions within Social Security, nuances within the system can cause confusion. A great example of this is how the rules about the Social Security cost of living adjustment affects spousal benefits.

To understand this calculation, and how to do it properly, requires a broad understanding on how the spousal benefit is calculated.

Financial advisors need to maintain knowledge and expertise about a wide range of planning topics. Most of them tackle this challenge well, and are able to speak on a number of different areas of finance and investing that matter most to their clients.

But one area that often gets neglected: Social Security.

If you’re a financial advisor or any other professional who works with individuals on some aspect of their financial life, I want to give you 3 reasons you need to seriously consider becoming the go-to expert on Social Security. Doing so will not only deepen your relationship with your current clients, but also equips you to achieve explosive growth in your practice.

Many of the nation’s successful small businesses are owned and operated by married couples. When these businesses first start, the goal is simply to try and survive to the next day, the next week, the next month.

Often, very little thought is given to the long-term effect of how self-employment income (abbreviated for our purposes here as SEI) is allocated for future Social Security benefits.

But under the right circumstances, planning in this area can make a big difference!

If you are reading this and are thinking, “I wish I would have known this sooner!” don’t despair. In the right circumstances, there may be an opportunity to retroactively amend the split of SEI for couples in this situation. We’ll cover more on that later.

For now, let’s start by understanding what couples who run a business together need to understand about how their pay structure could impact their future Social Security benefits.

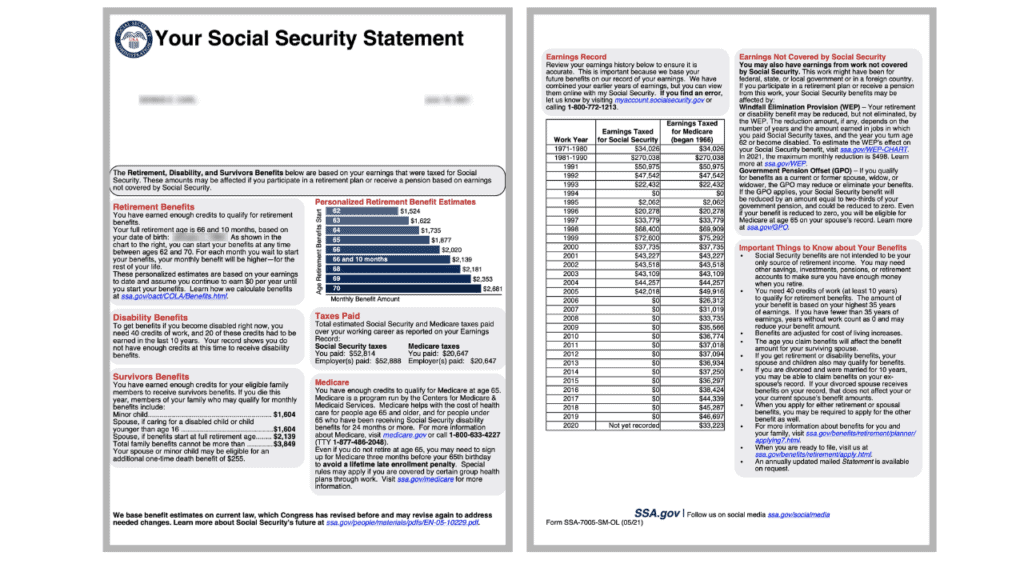

The Social Security monthly benefits statement that most people are familiar with has been around since 1999. That means we’ve been looking at the same Social Security statements for the last 22 years… and it’s high time the Social Security Administration gave their paperwork a modern makeover.

They did just that recently, and I want to walk you through what to expect when you see this new format come to you in the near future. While some people began receiving the new Social Security statements in May, the rollout is still in progress – so don’t be surprised if your statement still looks the same as it always has.

Once you do get your hands on the newest version, you may notice there are a few elements that you’re probably used to seeing that will no longer be included. Meanwhile, other aspects of the statements are brand-new and you want to make sure you fully understand those.

Young or old, you’ve likely heard of Social Security. You may even have some experience with it while planning your retirement or helping relatives navigate the complexities of Social Security, disability, or Medicare.

But why was the Social Security Act created? And how does it work today? Let’s look at the Social Security history timeline and how the benefits could impact your financial future.

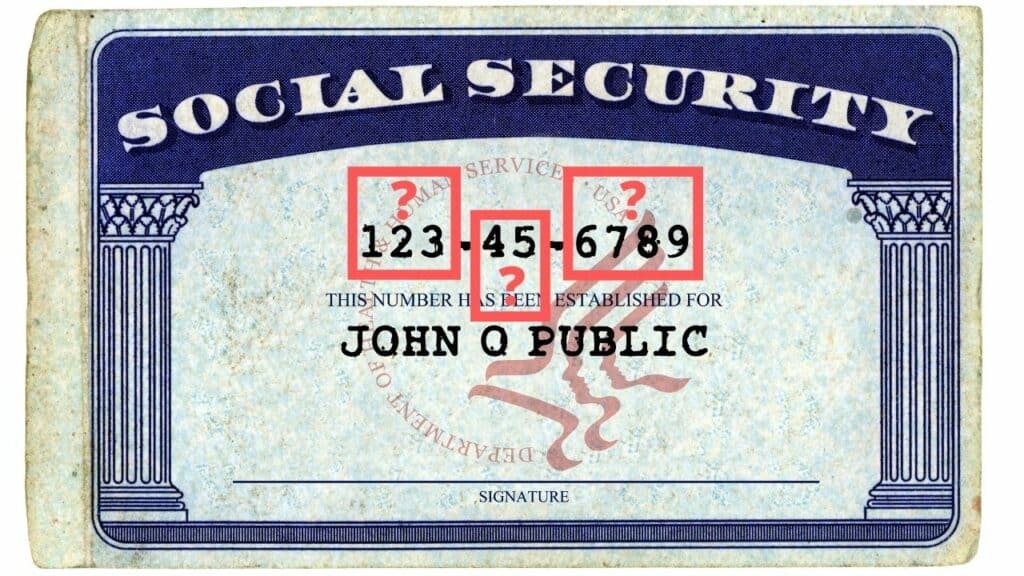

If you’ve ever applied for a job, loan, or credit card, you’ve probably been asked for your Social Security number. In many ways, your Social Security number is as much a part of you as your date of birth—it follows you from birth to death and can serve as a key to your sensitive information.

It’s clear that having one is vital because it’s used in various ways. You probably even know the number by heart. But have you ever wondered what Social Security numbers mean?

In this guide, discover what a Social Security number is, how to decode the numbers, if they’re reused, and what your number says about you.

Have you ever worked in a government job where you didn’t pay Social Security taxes? If that job also allowed you to earn a pension, then it’s critical that you understand the Government Pension Offset, or GPO.

The Government Pension Offset rule can drastically reduce, or even completely eliminate, your Social Security spousal or survivors’ benefits. That’s why it’s so important that if you ever worked in a public service job and earned a pension from your position, you take the time to learn everything you can about the GPO and how it could impact your Social Security income.

The Government Pension Offset’s mechanics are really simple: Your survivors’ or spousal benefits from Social Security will be reduced by an amount equal to two-thirds of your gross pension.

That’s a nasty surprise for the people who didn’t know about it, or fully understand how to plan for it. To avoid finding yourself in that situation, education is key. I’m sharing the top 7 questions I receive about the Government Pension Offset to help provide just that, so you can better plan for a successful retirement.

Figuring out when you and your spouse will each take Social Security retirement benefits can be a complex decision with unintended consequences. It’s important to understand how each spouse’s claiming decisions can affect you both. That’s why it’s important to think through your claiming strategies before either of you are ready to retire.

Here are three questions that can help you make the best decisions for your Social Security benefits individually and as a couple: