The gradual phase-in of taxes on Social Security benefits can deliver some unexpected and unpleasant results if you fail to recognize the “danger zone” to avoid. The calculation the IRS uses to determine how to tax Social Security income creates a category where taxes on benefits are amplified.

Fall into this danger zone, and you could pay a much higher tax rate on some of your retirement income. Here’s what you need to know about the taxes on Social Security benefits and how you can avoid the pitfall of paying way too much in taxes on that income.

Know Which Category You’re in for Taxation

Individuals fall into three basic categories for taxation on Social Security:

- None of your benefit is taxable income

- Between 0% and 85% of your benefit is taxable income (this is the danger zone!)

- 85% of your benefit is taxable

In the first category, you have no real need to fear slipping into the danger zone unless you have other income that could push you into the second category.

If you’re in the third category, you have few options to exercise to pay less in taxes.The only real choice you have is to somehow lower your reported income so that you qualify for the first or second category.

This is probably unrealistic, as people who find themselves in the third category are there thanks to large incomes from pensions, required minimum distributions, or some other source. You may need to accept that 85% of your benefit is taxable.

But if you find yourself in the second category, you may have more control over how much of your benefit is taxed.

Understanding the Danger Zone

I call that second category the danger zone because this is where taxes can nearly double on income.

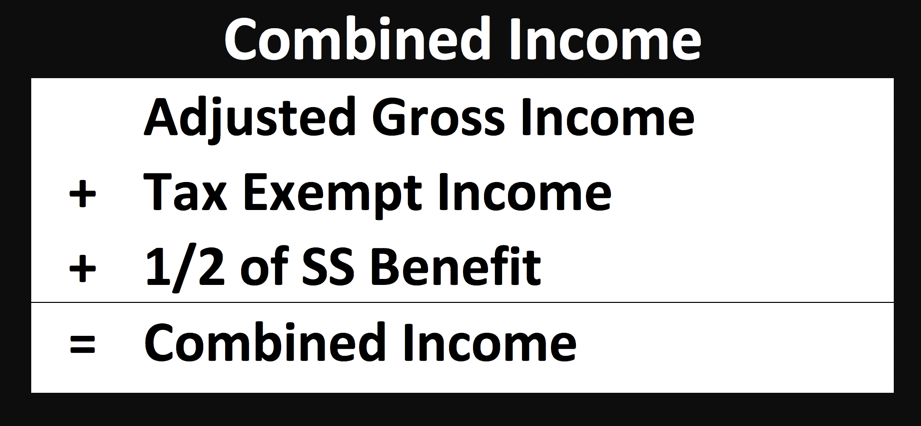

For some, this “danger zone” of magnified taxes can easily be avoided with a strategic, well-thought retirement income plan. The first thing you need to be able to do is to calculate your combined income.

This is the number the Social Security Administration uses to determines how much of your benefit is taxable. It’s also referred to as “provisional income,” but we’ll use the specific term combined income since the Social Security Administration uses that term.

Combined income can be roughly calculated as your adjusted gross income, plus any tax exempt interest (such as interest from tax free bonds), plus 50% of your Social Security benefits.

Once you’ve calculated your combined income you can apply it to the threshold tables to determine what percentage, if any, of your Social Security benefit will be included as taxable income.

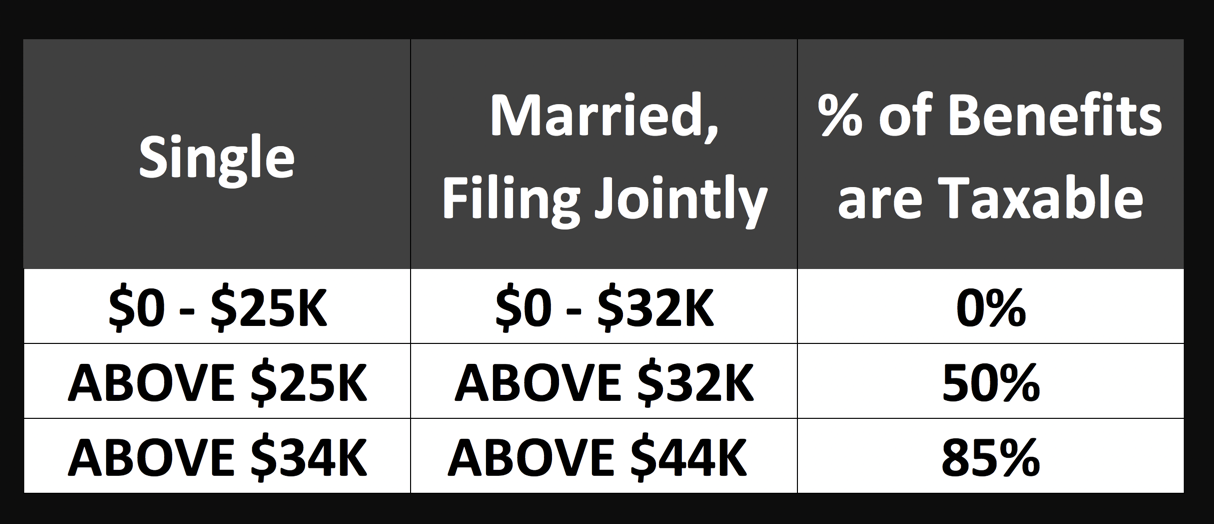

Thresholds for Social Security Taxes If You File Single

If your total combined income is less than the base amount of $25,000, none of your Social Security benefits will be taxed. But if your combined income is between $25,000 and $34,000, up to 50% of your benefit may be taxed.

If your combined income is more than $34,000, up to 85% of your benefits may be taxed.

Thresholds for Social Security Taxes If You’re Married Filing Jointly

If you file a joint return and you and your spouse have a combined income that is less than the base amount of $32,000, none of your benefits will be taxable.

If your total combined income is between $32,000 and $44,000, up to 50% of your benefit is taxable.

If your combined income is more than $44,000 up to 85% of your benefit may be taxable.

This system is a gradual phase-in of tax on Social Security benefits where, as income rises, more of your Social Security benefits are subject to taxation, until eventually a maximum of 85% of all benefits are subject to taxation.

For a more in-depth reading check out my article on the taxation of Social Security benefits.

What Happens to Social Security Taxes in the Danger Zone

Because of the way Social Security income phases into taxation through this formula, there is a “danger zone” when every dollar of increase in combined income pulls more Social Security into taxation.

In this zone, the effective tax rate on this other income skyrockets. For example, if an individual is in the upper end of the danger zone and takes $1.00 from his IRA account, they’ll not only have to pay tax on that $1 but also on $.85 of their Social Security benefit.

Effectively, because they took out $1 they had $1.85 added to their taxable income. This has the effect of increasing the marginal tax rate well beyond what your tax bracket might suggest you are paying.

If your tax bracket is 25% you would ordinarily pay $0.25 on the dollar you took out of your IRA. However, since that $1 increased your taxable income by $1.85, you will have to pay $0.46 in taxes. Since that $0.46 in taxes is solely due to your $1 distribution, you’re paying a 46% tax rate on that dollar!

This whole effect has been referred to as the tax torpedo — but for purposes of this article we’ll refer to it as the “danger zone” since my goal is to help you identify a specific range of provisional income where one should be hyper-vigilant about the effect of taking IRA distributions.

The danger zone ends when the results of your combined income calculation reaches 85% of your social security benefits. At this point, 85% of your benefit will be taxable, so increased combined income will not have the magnified effect.

For example, if you take $1 in IRA distributions it will not expose an additional $0.85 of Social Security benefits to taxable income since your benefit is already taxable.

Also, since all Social Security benefit amounts are not the same, the point where the danger zone ends will be different for everyone. Below we’ll break down the different ranges for those married filing jointly and those filing single.

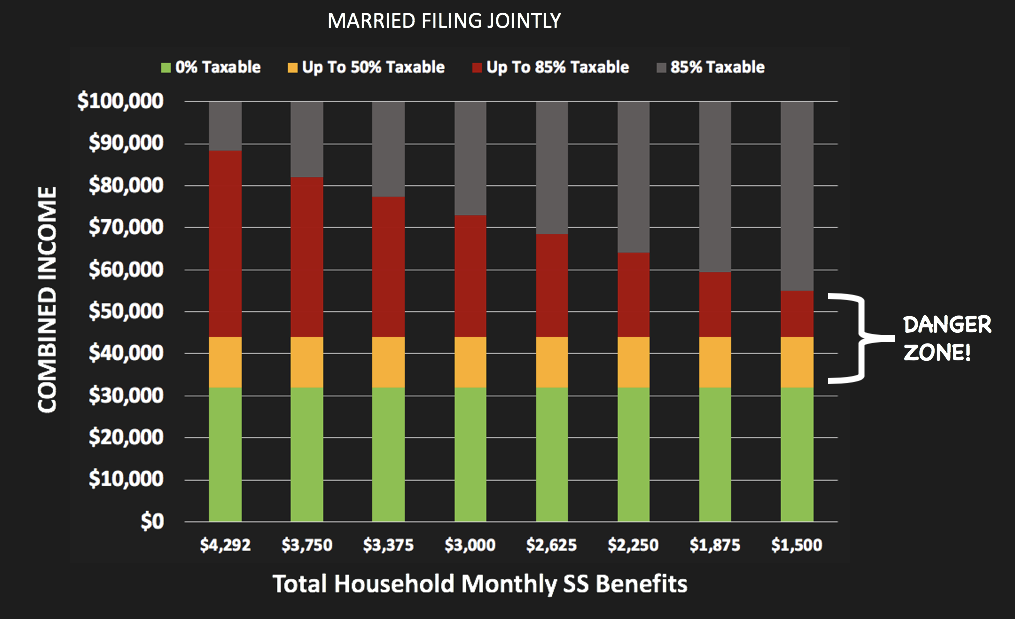

Where the Danger Zone Ends If You’re Married Filing Jointly

For those who are married filing jointly, exercise caution when combined income income rises over $32,000. At this point, your Social Security benefit will be added to your taxable income at the rate of $.50 for every additional dollar in combined income (signified by yellow on the chart below).

At $44,001 of combined income, your Social Security benefit will begin to be included in taxable income at the rate of $0.85 for every additional dollar in combined income (see the red areas of the bars in the chart below).

You’ll notice that the point at which someone can exit the danger zone varies based on the benefit amount. This is because the exit point is the point where the full 85% of your benefit becomes taxable.

The danger zone ends for those who are married filing jointly at around $88,000 for those who have a maximum benefit in 2019 and half of their benefit is being paid as a spousal benefit.

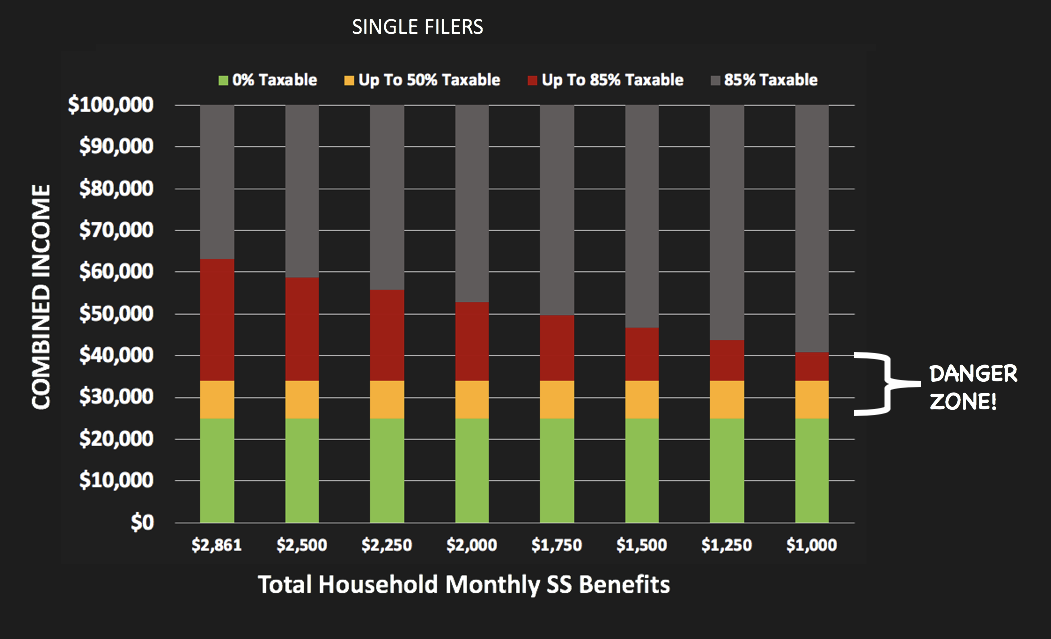

Getting Out of the Social Security Taxes Danger Zone for Single Filers

You need to start paying attention when your income rises above $25,000. At this point, your Social Security benefit will be added to your taxable income at the rate of $.50 for every additional dollar in combined income (signified by yellow on the chart below).

At $34,001 of combined income, your Social Security benefit will begin to be included in taxable income at the rate of $0.85 for every additional dollar in combined income (see the red areas of the bars in the chart below).

The danger zone ends for single filers around $63,000 in combined income for those with a maximum benefit (2019). For individuals with lower benefit amounts, you’re in the clear sooner.

The Opportunity Zone

In some cases, there is nothing to be done that will help lower the amount of taxes on Social Security. It could be due to required minimum distributions, pensions or a variety of other income sources.

Whatever the reason, some people will simply have incomes that are too high to make it possible to lower back into a zone of less than 85% Social Security taxation.

However, there are opportunities for planning around this danger zone. This opportunity not only exists for those who are in the danger zone, but also for those just over or under the line of the danger zone.

For those just over the line, it may be possible to defer capital gains, IRA distributions, or some other type of income if you could reduce the percentage of your taxable Social Security income by a few points.

Fully understanding how much range you have before Social Security benefits become taxable can be a big help in making choices about realizing capital gains, extra income from a job, or even deciding what type of account to use to fund your travel plans.

If you’re inside the danger zone, be aware that any increase in combined income will have an amplified effect on taxation. Instead of waiting until you are in that zone, there are a few steps you can take before it becomes an issue.

For starters, consider using a Roth IRA. This is possibly the most valuable tool for planning around tax on Social Security. Why? Distributions from a Roth are not counted in your combined income!

If you think you may eventually be in this danger zone, consider building a pool of money in your Roth account. You may be able to contribute to a Roth IRA up to $6,000 ($7,000 if over the age of 50).

Check with your retirement plan at work, as well, to see if they offer a Roth option. Using a Roth in 2019 will allow you to put in up to $19,000 per year ($25,000 if over the age of 50).

Finally, you may want to consider converting traditional IRAs to Roth IRAs. There’s certainly a lot to consider when doing so, but since the tax benefits could extend beyond the tax free nature of the Roth, this could be a winning move.

One thing is for sure, planning your retirement income stream is worth the effort! If I can be of assistance, please contact me at https://devincarroll.com/contact/

One last thing, be sure to get your FREE copy of my Social Security Cheat Sheet. This is where I took the most important rules and things to know from the 100,000 page Social Security website and condensed it down to just ONE PAGE! Get your FREE copy here.

One last thing…I’d like to give a huge thanks to two individuals who helped me with this article. Jim Blankenship, CFP, EA for his expertise on taxation and social security and Brandon Renfro, Ph.D. for his assistance on the research behind these calculations.